Vulnerability of supply chains exposed as global maritime chokepoints come under pressure

The latest Review of Maritime transport urges action to strengthen infrastructure and operations, promote low-carbon shipping and combat growing concerns over fraudulent ship registrations.

The global economy, food security, and energy supplies are at increasing risk due to vulnerabilities at key maritime routes. The Review of Maritime Transport 2024 from UN Trade and Development (UNCTAD) reveals that critical chokepoints – such as the Panama Canal (connecting the Pacific and Atlantic Oceans), the Red Sea and the Suez Canal (linking the Mediterranean Sea to the Indian Ocean via the Arabian Peninsula), and the Black Sea (an important hub for grain exports) – are under severe strain. A combination of geopolitical tensions, climate impacts, and conflicts have shaken global trade, threatening the functioning of maritime supply chains.

Maritime trade, which grew by 2.4% in 2023 to reach 12,292 million tons, began to recover after a contraction in 2022. However, the future remains uncertain. The report projects a modest 2% growth for 2024, driven by demand for bulk commodities like iron ore, coal, and grain, alongside containerized goods. Yet, these figures mask deeper challenges. Container trade, which grew by just 0.3% in 2023, is expected to rebound by 3.5% in 2024, but long-term growth will depend on how the industry adapts to ongoing disruptions, such as the war in Ukraine and rising geopolitical tensions in the Middle East. Meanwhile, the supply of container ship capacity grew by 8.2% in 2023. Disruptions at key maritime chokepoints, which temporarily increased demand for ships by lengthening shipping routes, have helped ease the issue of overcapacity. However, if shipping routes return to normal, the imbalance between supply and demand could lead to container vessel overcapacity.

Disruptions at major maritime chokepoints

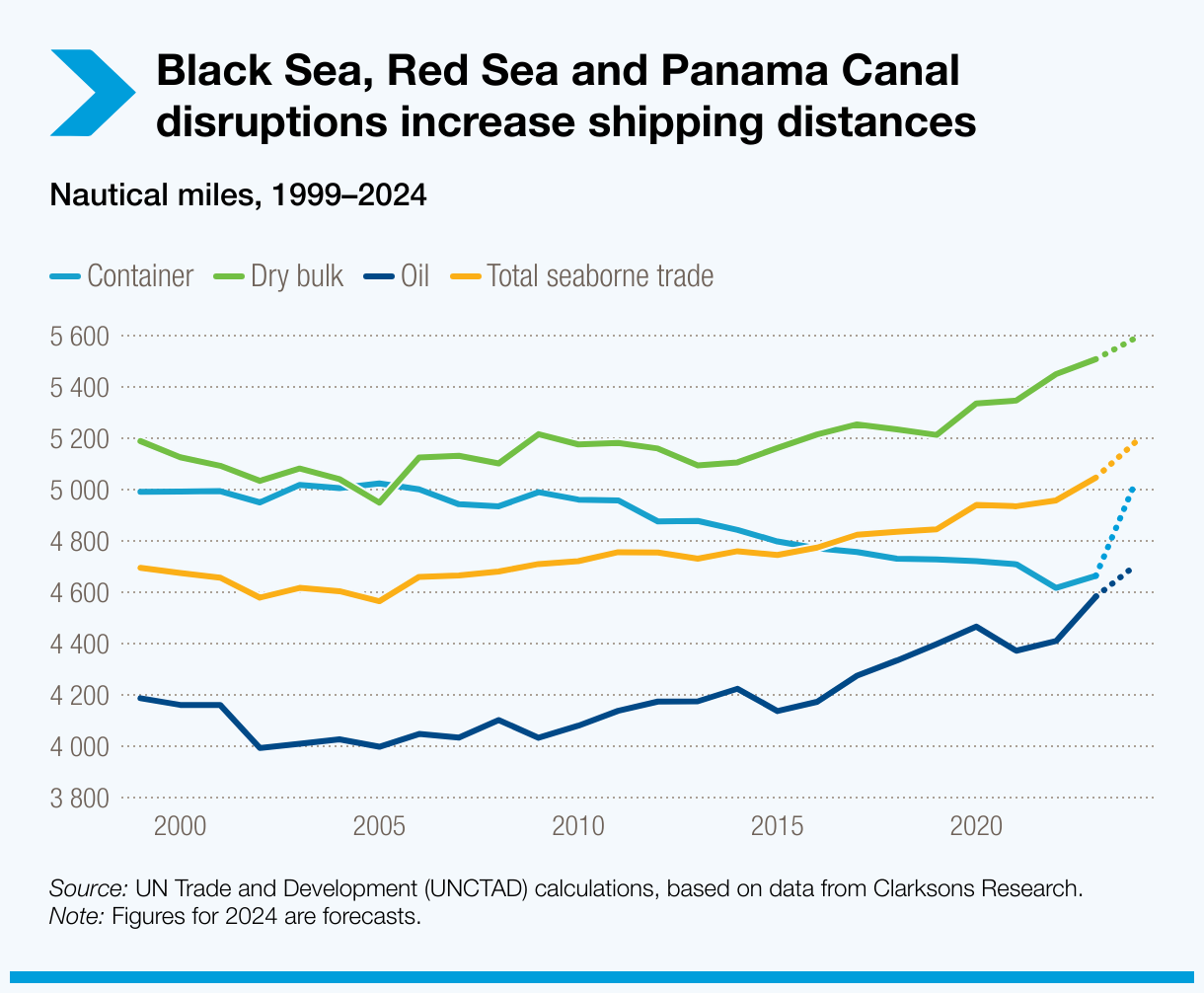

Key shipping routes have faced significant disruptions, causing delays, rerouting, and higher costs. Traffic through the Panama and Suez Canals – critical arteries of global trade – dropped by over 50% by mid-2024, compared to their peaks. This decline was driven by climate-induced low water levels in the Panama Canal and the outbreak of conflict in the Red Sea region affecting the Suez Canal. Meanwhile, the tonnage of ships transiting through the Gulf of Aden and the Suez Canal fell by 76% and 70% respectively, compared to late 2023.

![]()

Cargo rerouting around the Cape of Good Hope (southern tip of Africa) has surged, with ship capacity arrivals increasing by 89%. While this helps maintain the flow of goods, it adds significantly to costs, delays and carbon emissions. For example, a typical large container ship carrying 20,000–24,000 twenty-foot equivalent units (TEUs) on the Far East-Europe route incurs an additional $400,000 in emissions costs per voyage under the European Union’s Emissions Trading System (ETS) when diverting around Africa instead of using the Suez Canal.

Longer routes, higher costs

These longer routes have led to increased port congestion, higher fuel consumption, crew wages, insurance premiums, and exposure to piracy. Global ton-miles rose by 4.2% in 2023, driving up costs and emissions. By mid-2024, rerouting vessels away from the Red Sea and Panama Canal had increased global vessel demand by 3% and container ship demand by 12%, compared to what it would have been without these disruptions. This added significant pressure to global logistics and strained supply chains.

Port hubs like Singapore and major Mediterranean ports are now under pressure, as they cope with growing demand for transshipment services due to the rerouting of vessels. Congestion in these ports is adding another layer of complexity for global transport and trading networks.

Small island states and vulnerable economies hit hardest

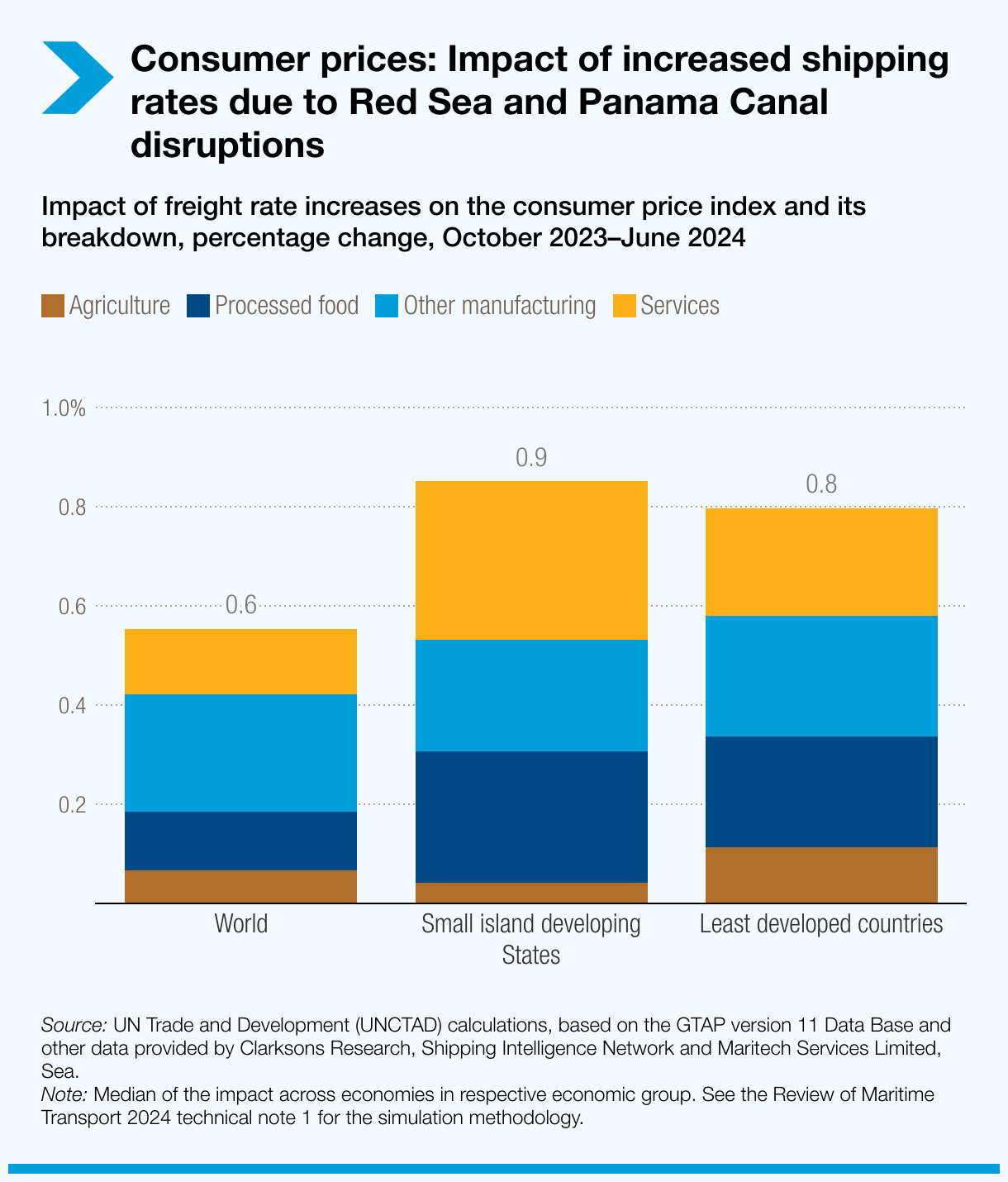

The disruptions and rising costs are not affecting all countries equally. Small Island Developing States (SIDS) and Least Developed Countries (LDCs) are experiencing the worst impacts. An analysis suggests that if the rise in container freight rates observed between October 2023 and June 2024 and caused by the disruptions in the Red Sea and Panama Canal continues until the end of 2025, global consumer prices could rise by 0.6% by the end of 2025. For SIDS, the potential impact is even more severe, with prices increasing by 0.9%, and processed food prices possibly rising by 1.3%.

SIDS economies rely heavily on shipping for essential imports, but their maritime connectivity has declined by 9% on average over the past decade, making their isolation more pronounced. Today, on average, SIDS are ten times less connected to global shipping networks compared to non-SIDS countries.

Adapting to climate change and building resilience to wide-ranging disruptions

The report highlights the urgent need for the maritime industry to build resilience against the growing impacts of climate change and other disruptions. Extreme weather events are disrupting port and shipping operations more frequently, posing safety risks, delaying operations and transit times and driving up costs. These disruptions also have legal implications, as companies must now factor climate risks into shipping contracts – to minimize losses and legal disputes, keep trade flowing and insurance affordable.

Building resilience across maritime chokepoints, transport and logistics in the face of multiple disruptions requires a comprehensive sector-wide approach. This includes capacity building and investments in infrastructure, services, workforce development, technology, partnerships and collaborative initiatives.

Accelerating the shift to low-carbon shipping

With global emissions continuing to rise and the International Maritime Organization (IMO) adopting more ambitious greenhouse gas emission targets in 2023, the need for rapid decarbonization is critical. However, progress remains slow as the transition to greener ships and low carbon fuels is still in its early stages. Fleet renewal has been hampered by uncertainty over future fuels and technology. By early 2024, only 50% of new ship capacity orders were for vessels capable of using alternative fuels. Meanwhile, scrapping older ships has slowed due to the high freight rates and increased demand for vessels following the rise in shipping distances.

Addressing fraudulent ship registration

Another pressing issue is the rise of fraudulent ship registrations and registries, undermining safety, security, pollution control, and seafarer welfare. This is compounded by a growing “dark fleet” of ships that operates under the radar, bypassing international regulations. UNCTAD calls on United Nations Member States and industry stakeholders to actively support IMO work to combat these fraudulent practices.

Key recommendations

As the maritime industry faces growing challenges, UNCTAD’s report urges coordinated efforts to navigate, adapt and thrive in this complex environment. It calls for addressing disruptions at maritime chokepoints, investing in low carbon and green shipping, enhancing port efficiency and adaptation, mainstreaming trade facilitation to improve hinterland connectivity and combating fraudulent ship registration. Additionally, the report emphasizes the importance of monitoring freight market developments, assessing trends in shipping rates and their impacts supporting vulnerable economies. By taking these steps, countries and their maritime industries can build a more resilient and sustainable future.